Investment, Insurance, Superannuation

APEX Insights > Inspire > Where in the world are advisers respected?

26 April 2018

Where in the world are advisers respected?

It’s not just you, around the world, financial advisers face challenges in communicating the value of their services to the general population.

And because that value is not understood, many consumers who could benefit from financial advice do not seek it out.

Australians’ uptake of investment advice is relatively low by global standards, although different definitions and research methodologies make it difficult to accurately compare across countries.

But it is interesting and insightful to understand how different nationalities perceive and take up advice. Because those differences are remarkable.

Advice take up in Australia

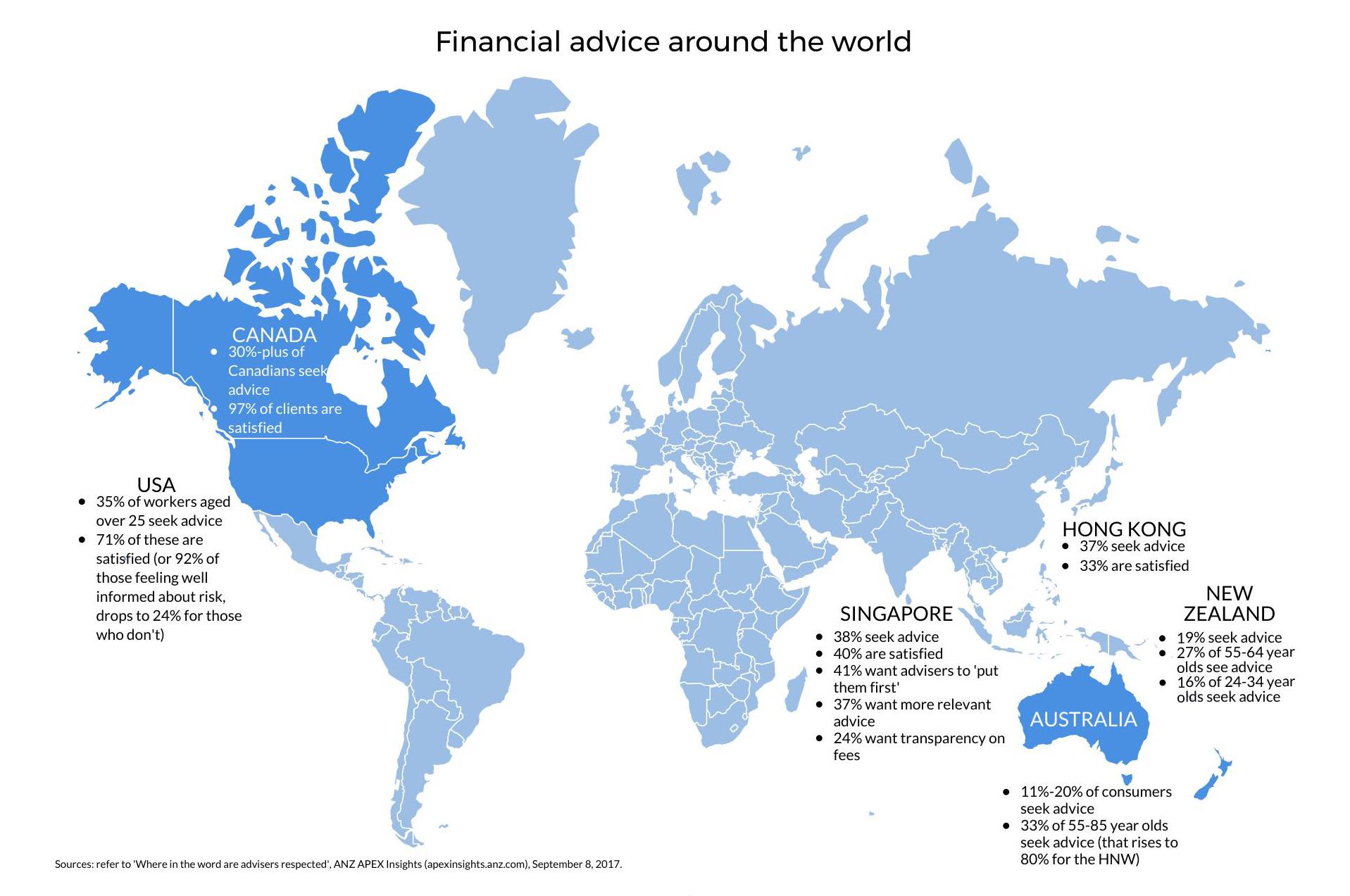

About 20 per cent of local consumers seek financial advice, according to the Financial Planning Association of Australia, although some estimate the figure could be as low as 11 per cent to 13 per cent.

Older Australians are more likely to seek advice than younger people, as are those with more money to invest.

About one third of people aged between 55 and 85 would speak to a financial adviser or planner when making financial decisions, a recent survey by the Australian Securities and Investments Commission found. A further 21 per cent would seek advice from an accountant or tax adviser.

Wealthy people in that age group were most likely to seek professional advice – about 80 per cent of those surveyed – compared with 39 per cent of people with fewer financial resources.

Advice take up around the world

Compared with Australia, a greater proportion of people in North America, and several Asian and European countries use financial advisers or planners.

In the USA, 35 per cent of working adults aged over 25 use a professional adviser, research by KRC Research for the Certified Financial Planner Board of Standards found. And most clients – 71 per cent – according to a separate survey by fund manager BlackRock – are highly satisfied with the service they receive.

New Zealanders seek advice at a similar rate to Australians, while participation rates for investment advice are lower in Britain and South Africa (although South Africa has one of the world’s highest take-up rates for life insurance).

Financial advice around the world: click to view infographic

What makes a client satisfied?

In the previously mentioned survey by BlackRock there was one startling fact – client satisfaction was down to one factor – how well informed they felt about investment risk.

Of clients who felt well informed about portfolio risks, 92 per cent were highly satisfied, compared with only 24 per cent of those who did not feel well informed. And that's down to the quality of communication from their adviser.

Strong adviser communication skills contributed to high client-satisfaction levels in Canada too.

Almost 80 per cent of Canadian investors – who make up 39 per cent of the total population – seek professional advice for all or some of their financial decision making, according to a survey by Gandalf Group, commissioned by AGF Management. This suggests more than 30 per cent of all Canadians use a financial planner or adviser.

The same survey found 97 per cent were either satisfied or very satisfied with their adviser. The high ratings resulted from advisers:

Poor adviser communications resulted in low levels of client satisfaction in Asia, although a large proportion of consumers in the region seek financial advice anyway.

In Hong Kong, 37 per cent of consumers use a financial adviser, but only one-third are satisfied with the service due to a lack of communication on fees and investments, BlackRock’s research showed.

Similarly, in Singapore, 38 per cent use an adviser but just two out of five are satisfied.

Trust was a major concern for Singaporeans, with 41 per cent saying they would have a higher opinion of advisers if they could find one who would put their [the client’s] interests first. Some 37 per cent said advisers would need to provide advice that was more relevant to them, and 24 per cent said advisers would have to more clearly disclose fees and commissions.

Articulating value

Fee disclosure and value for money are important to all consumers, regardless of location, age and level of wealth.

Almost three quarters of high-net-worth individuals surveyed in CapGemini’s Global HNW Insights Survey said lower overall fees and greater transparency of fees would encourage them to allocate more of their total financial wealth to their primary wealth-management professional.

Factors also critical to wealthy individuals around the world are:

Availability of advice

A lack of advisers, more than trust or fee issues, acts as a barrier to more New Zealanders receiving advice, according to a report by Kiwi Wealth.

With only 1800 authorised financial advisers available to serve 2.6 million KiwiSaver members (New Zealand’s voluntary long-term savings scheme), only 19 per cent of New Zealanders have a financial adviser, the report found.

As in Australia, older New Zealanders are more likely to seek assistance, with 27 per cent of people aged 55 to 64 using an adviser, compared with 16 per cent of 24 to 34 year olds, and just 6 per cent of those aged 18-24.

One solution that New Zealand – among other countries – is investigating to provide greater access to financial advice is robo-advice, which delivers automated but personalised financial assistance.

While technology will never entirely replace human advisers, many financial services businesses are using automated services to provide low-cost, accessible financial advice to a wider range of clients.

This material is intended for the use of financial advisers only and is distributed by OnePath Life Limited (OnePath Life) (ABN 33 009 657 176, AFSL 238341).

The information, opinions and conclusions in articles ("information") are current as at the date articles are written as specified within but are subject to change. The articles are provided and issued by OnePath Life unless another author is specified in the article, in which case it is provided and issued by that author. The views expressed are those of the authors only and do not necessarily reflect the opinions or views of OnePath Life, its employees or directors. Whilst care has been taken in preparing this material, OnePath Life and its related entities do not warrant or represent that the information is accurate or complete. To the extent permitted by law, OnePath Life and its related entities do not accept any responsibility or liability from the use of the information.

The information is of a general nature and has been prepared without taking into account a potential or existing investor’s objectives, financial situation or needs. Investors should consider whether the information is appropriate for them having regard to their objectives, financial situation or needs. For any product referred to above, OnePath Life recommends that investors read any relevant offer document or product disclosure statement and consider if the product is appropriate to them. For products issued by OnePath Life, these documents are available at access.onepathsuperinvest.com.au.

Past performance is not indicative of future performance and any case study shown is for illustrative purposes only. Neither are a prediction of the actual outcomes which will be achieved. Where tax or technical information is included, the information is our interpretation of the law and does not represent tax advice. An investor is advised to obtain professional advice relevant to their individual circumstances.